Model Validation

Models that are used by financial institutions need to be validated with regard to the soundness of modelling assumptions and the accuracy of implementation. We performed such model validation task on different levels including:

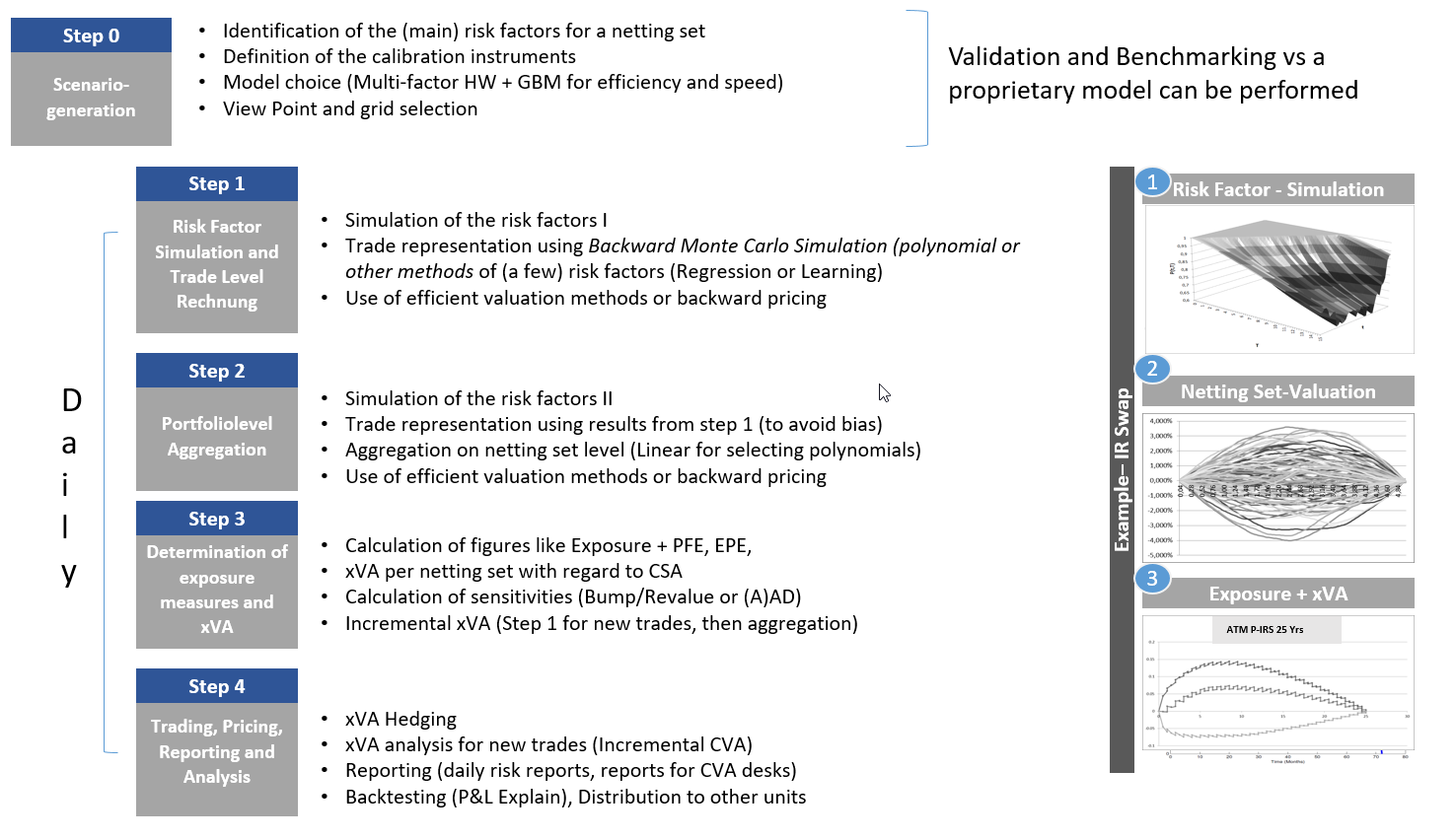

- CCR IMM – Validation of IMM approved methods for Counterparty Credit Risk (e.g. Two TIER I German bank) and for TRIM inspection (TIER I German bank)

- CCR IMM – Validation of an ‘to be approved’ new IMM method for Counterparty Credit Risk (TIER I German bank) including advanced stochastic volatility hybrid models

- xVA – Validation of a Front Office solution for xVA pricing (TIER I German bank) based on Machine Learning techniques to calculate exposure based measures and prices (CVA, DVA, FVA,…)

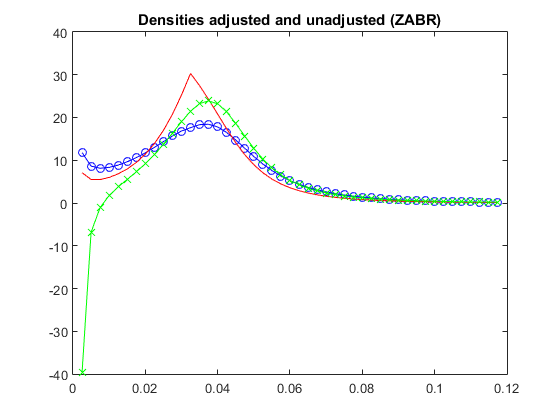

- Pricing methodologies for sensitivities for all asset classes, cash-settles swaptions, no-arbitrage

- SABR, Bermudan Swaption pricing assessment

- CMS and CMS Spread swaps pricing including derivatives such as Caps, Floors, Spread options.

Machine Learning / Statistical Methods

We applied statistical methods for time series analysis and deriving statistical properties relating to financial models including for instance dependency structures. Currently we investigate and implement the application of Machine Learning techniques to improve the performance and the accuracy of mathematical models applied to problems from finance. This includes

-

- Modern Lookup Tables for calibration and fast calculation of exotic prices involving deep learning techniques such as Forward Nets, Convolutional Nets, Recurrent Nets, etc.

- Gaussian Process Regression techniques

- CDS spread calculation for illiquid underlyings

Asset Allocation

We applied probablistic and advanced optimization techniques to many problems on asset allocation. All is based on a framework on multi-dimensional generalized hyperbolic distributions. This includes

- Selecting baskets from given investment universes to maximize a utility functions (yield, CPPI, etc.)

- Standard allocation using views (Black-Litterman, Opinion Pooling)

- Interest rate allocation for measuring performance for retail banking

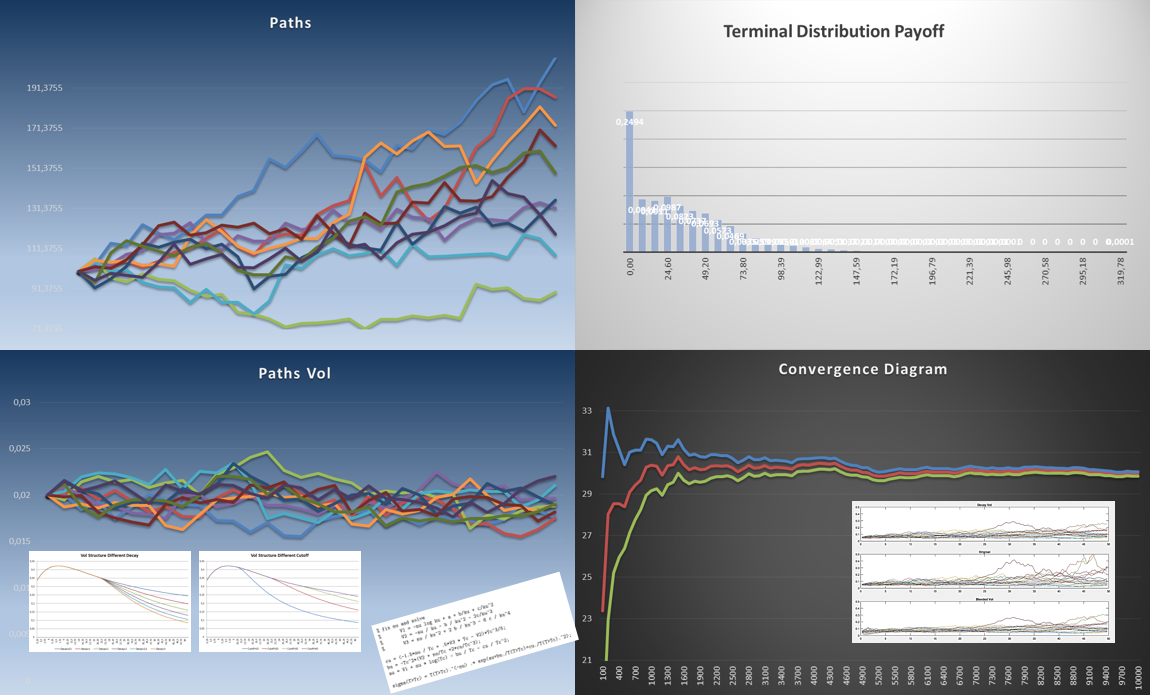

Economic Scenario Generation

Development of a model based on risk neutral valuation that covers Interest Rates (IR), Equitiy and Indicies (FX), Foreign Exchange (FX) and Inflation (INF). The models include

- The Heston-Hull-White Model

- Stochastic Volatility Libor Market Model for IR and INF combined with Heston models for EQ and FX

- Heath-Jarrow Mortong unspanned SV model for IR and Heston models for EQ, FX and CIR, OU model for Credit

- Volatility term structure modelling for market models for long dated contracts